Photo: Raflearning Lab

This article was originally published on Raflearning Lab.

Most of us have gotten caught in the rain without an umbrella or spent a morning commute sweltering in a heat wave. But for the millions of smallholder farmers around the world, the stakes run much higher than a soaked shirt. Weather is just one of many disruptive shocks that have the potential to destroy a crop and ruin a farmer’s season.

That’s where agricultural insurance comes in. By paying out after ‘occasional events with large economic impacts’, such as extreme weather and pest activity, agricultural insurance offers two potential benefits. First, it helps farmers avoid devastating financial losses in the event of a disruptive shock. Second, it limits the downside risk for smallholders investing in their own productive capacity. After all, if there is a good chance that new improved seeds won’t germinate because of drought, it can be hard to validate the extra expense. Insurance can ease farmers’ concerns about investing in technologies and improvements that are crucial for advancing their economic standing over time.

Sounds good, right? We think so too. ISF believes that agricultural insurance is an important financial service that both protects farmers and can help improve their productivity over time. And we’re not alone. In response to increasing market interest, and with the support of the Syngenta Foundation for Sustainable Agriculture, ISF developed a report entitled, “Protecting growing prosperity: Agricultural insurance in the developing world.” Now, six months later, we revisit the findings and provide an update on some of the recent developments in agricultural insurance since the report’s initial release.

Market overview: Agricultural insurance for smallholder farmers

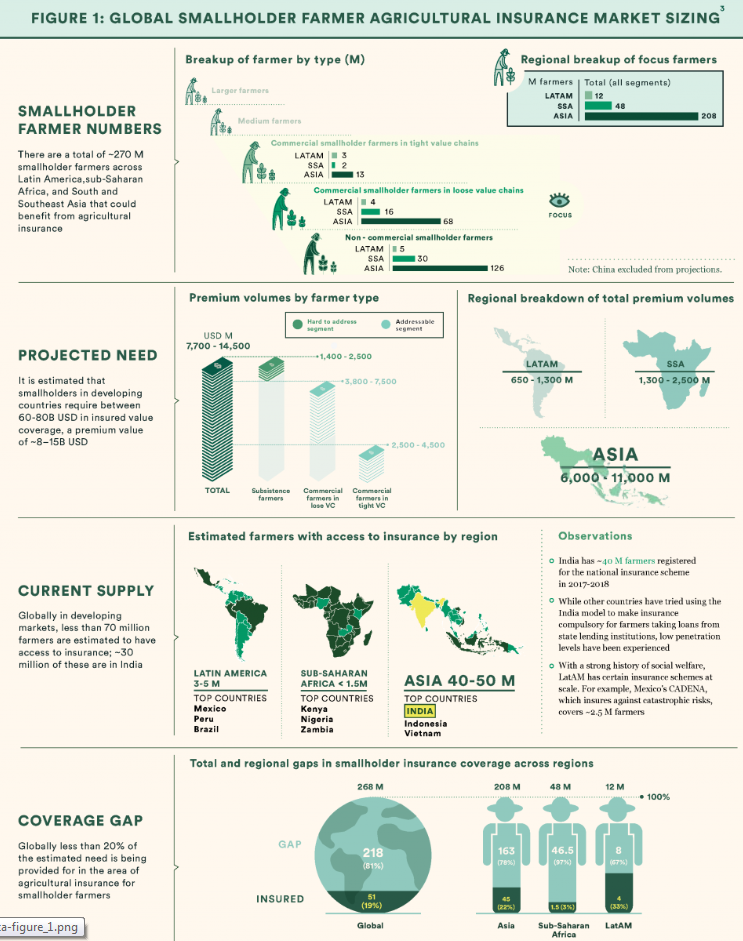

ISF estimates that globally less than 20% of smallholder farmers currently have agricultural insurance coverage, a number that is less than 3% in sub-Saharan Africa. Further, we estimate that ~270 million smallholder farmers in developing countries require USD 60-80 billion in agricultural insured value coverage. This amount of coverage represents an annual premium value of roughly USD 8–15 billion.

This coverage gap results from both low demand for and low supply of agricultural insurance products in developing nations. Smallholder farmers generally have low levels of understanding and trust in complex financial products. After all, the cost of insurance can be high and the payout mechanisms can be convoluted, slow, and divorced from the reality of a farmer’s actual losses. Meanwhile, developing, distributing, and servicing agricultural insurance policies in developing countries is complex and expensive for financial service providers.

Despite the challenges, agricultural insurance for smallholders represents a compelling market opportunity, from both a business and a social impact perspective. Accordingly, there is an increasing number of insurance products and schemes around the world trying to fill the coverage gap.

ISF conducted an inventory exercise classifying and examining ~100 agricultural insurance schemes in developing nations around the world. We found that traditional indemnity-based products are most prevalent in regions that have a history of strong public welfare systems, such as Latin America, Eastern Europe, and Central Asia.

However, these products have been difficult to implement in other regions. In the past ten years, advances in weather stations, satellite imagery, and risk modelling have driven a rise in index-based products, especially in Africa and South and Southeast Asia. These new insurance products track proxy data, such as rainfall or vegetation levels, to determine when a payout should be issued. Without a cumbersome claim assessment, these products can be offered at lower cost but have higher basis risk and rely on technology and skills that are currently lacking in many geographies.ISF believes that another 5-10 years of product and business model innovation is required to develop a robust, locally-tailored product class that meets the needs of both smallholder farmers and financial service providers.

Looking for leverage: How to move the market forward

Overall, our agricultural insurance landscape assessment paints a picture of an industry that shows great potential but is struggling to achieve the required scale and product-level refinements to graduate from the donor funding that has carried it to this point. The industry ‘ecosystem’ is complex, with many different actors facing systemic challenges. And while there is an emerging global agenda to develop this market, the solutions are highly dependent on national, or even subnational, context.

Our report identified four primary ‘leverage points’ that could accelerate the development of this crucial market:

Leverage Point 1: Governments engaged and equipped to drive the agenda

Leverage Point 2: A new step change in product effectiveness

Leverage Point 3: Product linkages that change the distribution and adoption game

Leverage Point 4: Coordinated global action

Market update: Big moves in agricultural insurance for smallholder farmers

Agricultural insurance for smallholder farmers is a complex market, and no single actor will be able to ‘solve’ the market constraints. Rather, we believe a more coordinated global agenda has strong potential to build momentum around early successes and innovate new approaches. A strong first step in that direction was taken in September 2018, when Syngenta Foundation for Sustainable Agriculture hosted a conference to bring together over 100 key stakeholders in the agricultural insurance ecosystem Download: Syngenta Foundation Agricultural Insurance Conference Report

Since that time, the industry continues to announce new initiatives and product innovations that are important steps forward in taking agricultural micro-insurance towards a tipping point. In Nicaragua, Incofin Investment Management (Incofin) is supporting two local microfinance institutions (MFIs) – Fundenuse and Micrédito – to implement the country’s first ever meso-model agricultural index insurance product. Meanwhile, in Uganda satellite-based drought insurance is expanding, and the ILO Impact Insurance Facility celebrated their 10-year anniversary by releasing a brief to share ten years of learnings regarding the successful provision of agricultural insurance in developing countries.