Photo: Agrilinks

Savings and Credit Cooperative Societies (SACCOs) are member-owned, democratically run, local financial service providers that play a critical role in the financial lives of farmers across sub-Saharan Africa. Farmers comprise 52% of members among the 176 government-regulated, deposit-taking SACCOs in Kenya. Many rural SACCOs started as farmer cooperatives or maintain close links with farmer groups that aggregate their produce for (usually cash-based) sales to agribusinesses. As such, SACCOs often have access to extensive data on their members’ agricultural production and sales. Most other financial service providers lack such community integration and remain reluctant to serve farmers — particularly geographically dispersed smallholders with limited or no land, collateral, formally documented income or credit history. As a result, millions of Kenyan farmers prefer to work with SACCOs and rely heavily on them for financial services that are key to their livelihoods.

Despite SACCOs’ proximity and close relationship with their members, it is still expensive to deliver frequent, small-scale financial services to widely dispersed farmers. Moreover, the farmers themselves confront high transaction costs — leading them to withdraw their savings all at once, for example, rather than travel frequently to the SACCO to withdraw small amounts as needed. With the rise of digital financial technology, or “fintech,” SACCOs now have an opportunity to improve their efficiency and transparency while also leveraging valuable farmer transactional data that has otherwise sat idle with the farmer cooperatives. Stakeholders seeking to increase rural financial inclusion should consider the role, potential and needs of SACCOs to expand the reach of digital financial and other services through their trusted, grassroots farmer networks.

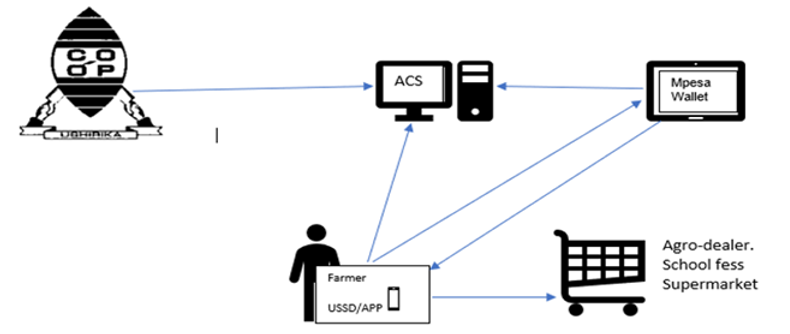

In an effort to enhance smallholder farmers’ access to finance, the Alliance for a Green Revolution in Africa (AGRA) partnered with Amtech Technologies Limited beginning in May 2018 to support the development of an automated credit scoring (ACS) application that enables farmers to access SACCO loans through their mobile phones. Amtech had already been developing information and communications technology (ICT) solutions for farmer cooperatives, including: EasyMa for farm produce intake by various value chain suppliers; EasySACCO, a core banking system for SACCOs; and Farm Level Management Data (FLMD) to enable farmer data profiles that fulfill know-your-customer regulations. With a grant from AGRA, Amtech developed a machine learning algorithm that bridges these three applications (EasyMa, EasySACCO and FLMD) to access and analyze up-to-date farmer data. Amtech’s cloud-based, data-sharing application then employs automated decision-making tools with SACCO-defined criteria to allocate farmer credit scores and approve loans according to defined credit limits. SACCO members are notified of their qualified credit limit via SMS messages and can apply for loans by dialing their SACCO’s Unstructured Supplementary Service Data (USSD) code on their mobile phone. Loan funds are disbursed within seconds to the farmer’s mobile wallet for immediate use. As of December 2020, this plug-and-play, cloud-based, data-sharing ACS had been implemented in 88 farmer-based SACCOs that are active in staple food, dairy, tea and coffee value chains in Kenya.

Schematic presentation of ACS as deployed by Amtech’s solutions.

The ACS has resulted in substantial gains in efficiency for both SACCOs and their members. Outcomes of this investment include:

-

Transaction turnaround time: The time taken to process a loan and make simple advances has been reduced from an average of seven days to under one minute.

-

Increased transactions: The SACCOs have registered notable increases in transactions. Since mobile phone penetration is high in most regions, SACCO members are using their phones to conduct more transactions. The ACS can conduct 500,000 transactions per day without crashing and has capacity for scalability.

-

Increased savings: Savings retention has increased because members tend to withdraw their funds digitally in small amounts only as they need them, as opposed to cashing out full balances in an effort to minimize trips to the branch.

-

Increased loans: The ease of access and rapid service provided by the ACS have led to growth in credit portfolios. As of the end of 2020, a total of 83,285 farmers had accessed over $12 million in credit through the ACS system across the 88 participating SACCOs.

-

Improved portfolio-at-risk (PAR): The 30-day PAR (PAR-30) of SACCOs implementing the ACS decreased from as much as 18% to under 2%.

-

Lower operational costs: The ACS reduces paperwork and staff time, thereby making the loan process less onerous and expensive for the SACCOs.

-

Farmer time savings and productivity: Instead of traveling to the SACCO branch, farmers can readily access banking information and transactions through their mobile phones — saving them valuable time, effort and transportation expense.

-

Lower SACCO traffic: Members used to crowd SACCO banking halls to conduct basic transactions, especially on paydays. The reduced traffic is allowing SACCO staff to concentrate on other tasks and improve service delivery.

-

More accurate data: The Bluetooth-enabled digital recordkeeping eliminates errors due to manual entry and estimations, thereby reducing data manipulation and disputes.

-

Data-based decision-making and controls: The ACS enables fairness and uniformity in credit decisions and administration by automating processes and avoiding loan officer bias.

-

Stronger customer communication: The ACS bulk SMS messaging platform enables the SACCOs to communicate efficiently and effectively with their members, which reinforces customer confidence and loyalty.

Over the course of the ACS design and implementation, AGRA and Amtech have collected a number of observations and lessons learned to guide ongoing innovation and scale-up:

-

SACCOs are enthusiastic about adopting technology that can keep them relevant and efficient, as well as sustain and attract new membership.

-

The SACCOs are interested in a system that can serve as a Credit Reference Bureau that helps them manage default risk by deterring member overindebtedness and preventing members from switching SACCOs without repaying their loans.

-

Many SACCOS are struggling with liquidity issues that prevent them from meeting the growing credit demands. Amtech is therefore seeking to crowd in more wholesale financial service providers on the basis of efficiency and operational gains afforded by the ACS.

-

High farmer training turnout indicates strong customer demand for capacity building. Bulk SMS and farmer education days during the SACCO Annual General Meetings can help keep training costs manageable while also meeting demand and reinforcing training outcomes.

-

SACCO board members also need training and capacity building on business strategy and investment during the transition to digital services. For instance, many SACCO members equate physical infrastructure as a sign of their cooperative’s stability and have expressed a desire to invest in bricks-and-mortar in remote areas as a response to membership and transaction growth. This is not necessarily an optimal use of scarce investment funds, and new technology requires new business approaches. Leadership capacity building can help hone future SACCO business strategy.

-

SACCOs need to protect themselves and their members from cybercrime, which can have huge impacts on individual farmers, as well as on the reputation of SACCOs and digital financial services among a population that may already be reticent. Amtech is providing training on cybercrime, anti-money laundering, bribery laws and consumer protection, and further investment is needed to reinforce cybersecurity.

As local, self-managed mutual interest groups, rural SACCOs have long played a central role in the lives and livelihoods of low-income farmers. Their loyal member networks represent meaningful scale in hard-to-reach areas, and their farm-level data presents a key to risk management for agricultural finance. As the financial inclusion sector looks for ways to ensure that the exclusion of rural smallholder farmers is not exacerbated by a digital divide, fostering SACCOs’ participation in the digital finance revolution can be a powerful step. Investments in digitization of SACCO operations, such as farm-level data collection, automated credit scoring, loan approval and transactions, hold promise for widespread uptake of digitally enabled financial and nonfinancial services. Equipping SACCOs with cutting-edge digital tools will reinforce sustainable service delivery and result in far-reaching impacts on farmers and the rural economy.

This article was originally published by Agrilinks.